Moving into a new apartment can be an exciting time, but it’s important to go into it with your eyes open. While rent is the most obvious cost, it’s far from the only one. From security deposits to utilities, there are many hidden expenses you need to consider when budgeting for your new home. This article will break down all the expenses you need to factor in when calculating the true cost of renting an apartment, helping you make a well-informed decision about your housing situation.

Understanding Base Rent

Base rent is the fundamental cost of renting a commercial property. It’s the monthly or annual fee a tenant pays for the right to occupy and use the space, excluding any additional charges. This core component of rent is typically determined by factors such as:

- Property Location: Prime locations with high foot traffic or desirable demographics command higher base rents.

- Property Size and Features: Larger spaces, unique amenities, and modern design often influence a higher base rent.

- Market Conditions: The overall supply and demand for commercial real estate in the area play a crucial role in setting base rents.

- Lease Term: Longer lease terms may sometimes lead to lower base rents as landlords seek long-term tenants.

It’s important to note that base rent doesn’t include additional expenses, often referred to as operating expenses. These can include property taxes, insurance, maintenance, utilities, and management fees. These expenses are typically passed on to the tenant through various methods like:

- Percentage Rent: A percentage of the tenant’s gross sales is added to the base rent.

- Additional Charges: Separate fees for specific services, such as parking or utilities.

- Gross Lease: The base rent includes all operating expenses, making it a fixed monthly payment for the tenant.

Understanding the distinction between base rent and operating expenses is vital for tenants when negotiating lease terms. By carefully analyzing the lease agreement and considering all potential costs, tenants can secure favorable financial terms for their business operations.

Factoring in Utilities

When buying a property, it’s crucial to consider the cost of utilities. These ongoing expenses can significantly impact your monthly budget and overall financial stability. To make informed decisions, it’s important to understand the different types of utilities, their potential cost variations, and how to factor them into your financial planning.

Types of Utilities

Here are some common utilities you’ll likely encounter as a homeowner:

- Electricity: Powers your lights, appliances, and electronic devices.

- Gas: Used for heating, cooking, and water heating.

- Water and Sewer: Provides access to clean water and wastewater disposal.

- Trash Removal: Disposes of your household waste.

- Internet and Cable: Provides communication and entertainment services.

Cost Variations

Utility costs can vary greatly depending on several factors:

- Location: Geographic location and climate can impact heating and cooling needs, influencing electricity and gas usage.

- Home Size: Larger homes generally consume more energy and water, leading to higher utility bills.

- Energy Efficiency: Energy-efficient appliances and insulation can help reduce your consumption and costs.

- Usage Habits: Your personal usage patterns, such as showering time or thermostat settings, affect utility consumption.

- Provider and Rates: Different utility providers offer varying rates and plans, impacting your costs.

Factoring Utilities into Your Budget

To effectively factor utilities into your financial planning, consider these steps:

- Research Utility Costs: Contact utility providers in the area you’re considering and inquire about average monthly costs.

- Estimate Usage: Assess your anticipated usage based on your lifestyle and the size of the property.

- Include Utilities in Your Budget: Allocate a realistic amount for utilities in your monthly budget, accounting for potential fluctuations.

- Explore Energy-Saving Measures: Consider installing energy-efficient appliances, improving insulation, and adopting energy-saving habits to reduce consumption.

- Review and Adjust: Regularly review your utility bills and make necessary adjustments to your budget as needed.

Conclusion

Factoring in utilities is a crucial step in the homebuying process. By understanding the types of utilities, potential cost variations, and how to budget effectively, you can make informed decisions and avoid unexpected financial burdens. By taking proactive measures to estimate costs, explore energy-saving opportunities, and adjust your budget as needed, you can effectively manage your utility expenses and enjoy a more financially stable homeownership experience.

Additional Monthly Expenses

When creating a budget, it’s important to account for all your monthly expenses. You might think that you have everything covered, but there are often a few additional expenses that slip through the cracks. These expenses might not be predictable, but they can add up over time and hurt your financial stability.

Here are some additional monthly expenses that you may not have considered:

- Gifts: Birthdays, holidays, and special occasions can all require you to spend money on gifts. Be sure to budget for these expenses in advance, especially if you have a lot of people to buy gifts for.

- Entertainment: Going out to eat, seeing movies, or attending concerts can all be expensive. If you enjoy these activities, be sure to budget for them.

- Subscriptions: Many people subscribe to services like streaming music or video, online storage, or fitness apps. These subscriptions can add up, so be sure to track them and cancel any that you don’t use.

- Home maintenance: Your home will require occasional repairs and maintenance. It’s important to budget for these expenses, even if they don’t occur every month.

- Pet care: If you have pets, you’ll need to budget for their food, supplies, and veterinary care. Be sure to factor in the cost of any unexpected medical bills.

- Personal care: This category includes expenses such as haircuts, manicures, and toiletries. These expenses might seem small, but they can add up over time.

- Unexpected expenses: Life is full of surprises, and you can’t always predict when you’ll need to spend money on unexpected expenses. It’s a good idea to have a small emergency fund to cover these costs.

By budgeting for these additional monthly expenses, you can help ensure that you’re not caught off guard by unexpected costs. This will help you to stay on track with your finances and achieve your financial goals.

Estimating One-Time Costs

One-time costs are expenses that are incurred only once, unlike recurring costs, which are incurred regularly. These costs can be significant, and it’s important to accurately estimate them to ensure that your project stays on budget.

Here are some common one-time costs that you may encounter:

- Initial setup costs: These costs are incurred when you first start your business or project, and can include expenses such as legal fees, permits, and licenses.

- Equipment costs: You may need to purchase equipment, such as computers, software, or machinery, to operate your business or complete your project.

- Marketing and advertising costs: You may need to spend money on marketing and advertising to promote your business or project.

- Training costs: You may need to train employees or yourself on how to use new equipment or software.

- Inventory costs: If you sell products, you will need to purchase inventory to stock your shelves.

- Research and development costs: If you are developing a new product or service, you may need to invest in research and development.

There are several methods you can use to estimate one-time costs:

- Research: Look at industry averages and benchmarks to get a general idea of what others are spending.

- Quotes: Get quotes from vendors for the goods and services you need.

- Historical data: If you have experience with similar projects, use your past data to estimate costs.

- Expert advice: Consult with experts, such as accountants, consultants, or project managers, for their insights.

Once you have estimated your one-time costs, it’s important to factor them into your overall budget. It’s also essential to have a contingency plan for unexpected expenses. This could include setting aside a percentage of your budget for unforeseen costs or having a source of emergency funding.

By carefully estimating your one-time costs, you can ensure that your project or business is financially sustainable.

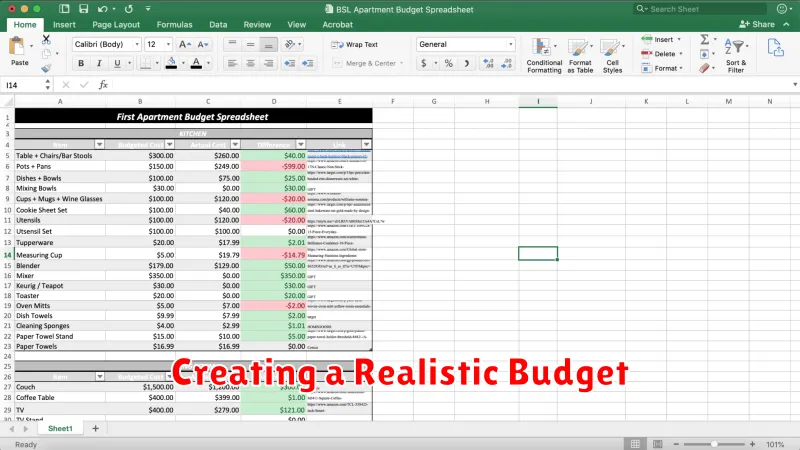

Creating a Realistic Budget

A budget is a plan for how you will spend your money. It can help you track your income and expenses, and make sure you are not spending more than you earn. Creating a realistic budget can be a challenge, but it is an important step towards financial stability.

Here are some tips for creating a realistic budget:

- Track your spending: The first step is to track your spending for a few months. This will give you a clear picture of where your money is going. You can use a budgeting app, spreadsheet, or even just a notebook to track your expenses.

- Create a spending plan: Once you know where your money is going, you can create a spending plan. This involves allocating your income to different categories, such as housing, food, transportation, and entertainment.

- Set realistic goals: When setting your budget, it is important to set realistic goals. Don’t try to cut your spending too drastically, or you may be more likely to give up. Start with small changes and gradually work your way up.

- Review your budget regularly: It is important to review your budget regularly and make adjustments as needed. Your financial situation may change over time, so it is important to stay on top of your spending and make sure your budget is still working for you.

- Automate your savings: One of the best ways to save money is to automate your savings. This means setting up automatic transfers from your checking account to your savings account. This way, you will be saving money without even thinking about it.

Creating a realistic budget can take some time and effort, but it is well worth it. A budget can help you achieve your financial goals, such as paying off debt, saving for retirement, or buying a home.

Tips for Reducing Rental Costs

Finding an affordable place to live can be a challenge, especially in competitive rental markets. But don’t despair! There are several ways to reduce your rental costs and make your budget stretch further. Here are some tips to consider:

Negotiate with Your Landlord

Don’t be afraid to negotiate with your landlord! Many landlords are open to discussing rent prices, especially if you’re willing to sign a longer lease or offer a security deposit. Be prepared to present a strong case, highlighting your reliability and good credit history.

Consider a Roommate

Sharing an apartment with a roommate can significantly lower your rental costs. This option can be a great way to split the rent and utilities while also building a social connection.

Look for Off-Peak Seasons

Rental prices tend to fluctuate throughout the year. Consider moving during the off-peak season, such as winter or early spring, when demand is lower and landlords may be more flexible with pricing.

Explore Different Neighborhoods

Sometimes a slight change in location can make a big difference in your rent. Consider exploring neighborhoods that are just outside the most popular areas. You might find comparable units at a lower price in a quieter location.

Research Rental Assistance Programs

Many cities and states offer rental assistance programs for low-income families and individuals. Check with your local government or housing authority to see if you qualify for any assistance programs.

Be a Responsible Tenant

Landlords are more likely to offer incentives to tenants with a good track record. Pay your rent on time, maintain the property, and respect the rules of the lease agreement. This can help you build a positive relationship with your landlord and potentially earn future benefits.

Negotiate Utilities

If your lease doesn’t include utilities, explore options for splitting costs with roommates or negotiating with your landlord to bundle some utilities into your rent.

Use Public Transportation

Living in a location with good public transportation can significantly reduce your transportation costs. This can free up your budget for other expenses.

By considering these tips, you can find affordable rental options and save money on your housing costs.

Hidden Costs to Consider

When making a major purchase, like a new car or a home, it’s important to consider not just the sticker price, but also the hidden costs that can quickly add up. These costs might not be immediately obvious, but they can significantly impact your overall budget. Understanding these hidden costs can help you make more informed decisions and avoid financial surprises down the line.

Here are some common hidden costs to keep in mind:

Financing Costs

When financing a purchase, the interest rate can significantly increase the total cost. Be sure to shop around for the best rates and compare different loan terms.

Insurance

The cost of insurance can vary widely depending on the item being insured, your location, and your individual risk profile. Make sure to factor in insurance premiums when calculating your overall costs.

Maintenance and Repairs

Even brand-new items require maintenance and repairs over time. Research the average cost of upkeep for the item you’re considering and set aside funds to cover these expenses.

Taxes and Fees

Many purchases come with additional taxes and fees, such as sales tax, registration fees, and closing costs. Don’t forget to factor these expenses into your budget.

Operating Costs

If you’re buying a car, for example, be sure to consider the cost of fuel, maintenance, and parking. These operating costs can add up quickly.

Opportunity Costs

Don’t forget about opportunity costs, the value of the next best alternative you’re giving up. If you spend a large sum of money on one purchase, you might miss out on other opportunities, such as investing or saving for retirement.

By considering all the hidden costs associated with a purchase, you can make more informed financial decisions and avoid potential financial surprises. It’s always better to be prepared and budget accordingly than to find yourself struggling to cover unexpected expenses.

{kind=link}