Finding an apartment can be stressful, but it doesn’t have to be! Rent-to-own apartments offer a flexible and affordable alternative to traditional renting, allowing you to build equity while you rent. This type of arrangement can be a great option for those who are working towards homeownership but aren’t quite ready for a traditional mortgage. Whether you’re looking for a rent-to-own apartment in your city or are just starting your search, this article will guide you through the process and provide valuable tips for finding the perfect rent-to-own property for you.

Understanding Rent-to-Own Agreements

A rent-to-own agreement, also known as a lease-purchase agreement, is a contract where a tenant pays rent for a property while also making payments towards an eventual purchase. It can be a good option for people who are unable to qualify for a traditional mortgage or who want to build equity in a home over time.

Here’s how a rent-to-own agreement works:

- The tenant pays monthly rent payments, which may be higher than a standard rental agreement, to the landlord or seller.

- A portion of the rent is applied towards a down payment on the property.

- The agreement usually includes a purchase option, which gives the tenant the right, but not the obligation, to purchase the property at a pre-determined price within a specific timeframe.

- If the tenant exercises the purchase option, they will need to obtain financing for the remaining balance of the purchase price.

Advantages of Rent-to-Own Agreements

Rent-to-own agreements can offer several benefits:

- Potential for homeownership: It gives individuals a path towards owning a home who may not be able to qualify for a traditional mortgage.

- Building equity: A portion of the rent payments goes towards the purchase price, allowing you to build equity in the property.

- Time to prepare: The agreement gives you time to improve your credit score and financial situation, making you more eligible for a mortgage later on.

Disadvantages of Rent-to-Own Agreements

Rent-to-own agreements also come with certain drawbacks:

- Higher rent payments: Rent payments may be higher than a standard rental agreement.

- Potential for loss of investment: If you decide not to purchase the property, you may lose the money you paid towards the down payment.

- Unfavorable purchase options: The purchase price may be higher than the market value, and the agreement might not be beneficial in the long run.

- Legal complexities: Rent-to-own agreements can be complex and require careful legal review before signing.

Considerations Before Entering a Rent-to-Own Agreement

Before entering a rent-to-own agreement, carefully consider the following:

- The purchase price: Ensure that the price is fair and in line with the market value.

- The purchase option period: Make sure you have enough time to secure financing and decide whether to purchase the property.

- The legal terms: Seek legal advice from a qualified attorney to understand the terms and conditions of the agreement.

- Your financial situation: Assess your financial situation and your ability to make the rent payments and eventually secure a mortgage.

Rent-to-own agreements can be a viable option for individuals seeking homeownership, but it’s important to thoroughly understand the benefits, risks, and legal complexities involved. Careful consideration and professional advice are essential to ensure a positive experience.

Benefits of Choosing a Rent-to-Own Apartment

In today’s competitive housing market, finding a place to call home can be a daunting task. Traditional homeownership often seems out of reach, with hefty down payments and stringent lending requirements. However, a rent-to-own apartment offers a unique and attainable pathway to homeownership.

Here are some compelling benefits of choosing a rent-to-own apartment:

1. Affordability

Rent-to-own apartments typically require a smaller down payment compared to traditional mortgages. This makes homeownership accessible to individuals who may not have the financial resources for a substantial upfront investment. Moreover, the rent payments often include a portion that goes towards the eventual purchase price, allowing you to build equity gradually.

2. Predictable Payments

With a rent-to-own agreement, your monthly payments are fixed for a specific period. This provides financial stability and allows you to budget effectively for your housing expenses. You won’t be subjected to sudden rent increases or fluctuating mortgage rates.

3. Time to Prepare

Rent-to-own agreements give you ample time to improve your credit score and financial standing. During the rental period, you can focus on building your savings and preparing for the eventual home purchase. This provides you with a valuable head start towards achieving homeownership.

4. No Closing Costs

Unlike traditional mortgages, rent-to-own agreements typically eliminate the need for significant closing costs. This saves you money and allows you to allocate more funds towards your down payment or home improvements.

5. Security and Stability

A rent-to-own agreement provides a sense of security and stability. Unlike renting a property, you have a guaranteed option to purchase the apartment at the end of the rental term. This eliminates the uncertainty of constantly searching for a new place to live.

However, it’s essential to carefully review the terms of the rent-to-own agreement before signing. Ensure that you understand the purchase price, the length of the rental period, and any other applicable fees. Consult with a financial advisor to assess your financial situation and determine if rent-to-own is the right choice for you.

Ultimately, choosing a rent-to-own apartment can be a strategic step towards homeownership. It offers a more manageable and flexible path to owning a piece of your own real estate. With careful planning and responsible financial management, you can achieve your homeownership goals and enjoy the security and pride of owning your own space.

Drawbacks to Consider

There are many benefits to using a solar panel, but it’s important to consider the drawbacks as well. One major drawback is the initial cost of installation, which can be significant. Additionally, solar panels are not always effective in cloudy weather, meaning you may still need to rely on traditional energy sources.

Where to Find Rent-to-Own Apartments

Rent-to-own apartments can be a great option for people who are looking to buy a home but aren’t quite ready to take the plunge. They offer the opportunity to build equity while living in a place you love, and they can be a good way to improve your credit score. But finding the right rent-to-own apartment can be tricky.

Here are a few places you can look for rent-to-own apartments:

- Real estate agents: Many real estate agents specialize in rent-to-own properties. They can help you find properties that meet your needs and negotiate the terms of your lease-purchase agreement.

- Online listings: There are a number of websites that list rent-to-own apartments. Some of the most popular include:

- Rent.com

- Apartments.com

- Zillow

- Trulia

- Local newspapers: Many local newspapers have classified sections that list rent-to-own properties.

- Word-of-mouth: Ask friends, family, and colleagues if they know of any rent-to-own apartments available.

Once you’ve found a few potential properties, it’s important to do your research before you sign anything. Be sure to ask the following questions:

- What is the purchase price of the property?

- What is the length of the lease-purchase agreement?

- How much of your monthly rent will be applied to the purchase price?

- What are the closing costs?

- What is the credit score requirement?

- What are the penalties for breaking the lease-purchase agreement?

It’s also a good idea to get a home inspection before you sign a lease-purchase agreement. This will help you identify any potential problems with the property.

Rent-to-own apartments can be a great option for some people, but it’s important to do your research and make sure you understand the terms of the agreement before you sign anything. By following these tips, you can increase your chances of finding a good deal on a rent-to-own apartment.

Essential Factors in a Rent-to-Own Contract

A rent-to-own contract, also known as a lease-purchase agreement, allows you to rent a property with the option to purchase it at a later date. While this can be a great way to build equity and eventually own your own home, it’s important to understand the key factors involved and the potential risks.

Key Considerations When Evaluating a Rent-to-Own Contract

- Purchase Price: The contract should clearly state the final purchase price of the property. This should be fair and reasonable, taking into account the current market value and any necessary repairs.

- Rent-to-Own Period: Determine the length of the lease-purchase agreement. This will dictate how long you’ll be renting before you can exercise the option to purchase.

- Option Fee: Understand the amount of the option fee, which is typically a non-refundable payment you make to secure the right to buy the property. This fee is usually a percentage of the purchase price.

- Credit Check and Approval: If you plan to purchase the property, be prepared for a credit check and approval process. Your credit score will likely influence the terms of the agreement.

- Inspection and Repairs: Before signing the contract, thoroughly inspect the property for any existing damage or needed repairs. The agreement should detail who is responsible for maintaining the property during the lease period.

- Escape Clause: Review the contract for an escape clause. This clause protects you in case you change your mind or are unable to purchase the property at the end of the lease-purchase term.

- Legal Counsel: It’s highly recommended to consult with an attorney before signing a rent-to-own agreement. They can help you understand the legal implications and protect your interests.

Advantages of Rent-to-Own

There are several advantages to a rent-to-own arrangement:

- Building Equity: A portion of your rent payments may be applied towards the purchase price, allowing you to build equity in the property over time.

- Time to Improve Credit: The rent-to-own period gives you time to improve your credit score, which could make it easier to secure a mortgage later.

- Avoid Bidding Wars: A rent-to-own agreement can lock in a purchase price, avoiding the competitive nature of the housing market.

Disadvantages of Rent-to-Own

There are also potential drawbacks to consider:

- Higher Costs: Rent-to-own agreements often involve higher monthly payments compared to traditional rentals, as a portion goes towards the purchase price.

- Loss of Option Fee: If you choose not to purchase the property, you’ll likely lose the option fee you paid upfront.

- Hidden Fees and Costs: Be aware of any hidden fees or costs associated with the agreement, such as repairs, insurance, or property taxes.

Conclusion

Rent-to-own can be a viable option for homeownership, but it’s crucial to carefully evaluate the contract terms and potential risks. Thoroughly understand the purchase price, lease-purchase period, option fee, inspection process, and your financial obligations. Consult with an attorney to ensure the agreement is fair and protects your interests.

Negotiating the Terms of Your Agreement

Negotiating the terms of an agreement is a crucial aspect of any business deal. It’s a process that requires careful consideration, strategic planning, and effective communication. Whether you’re a buyer or a seller, understanding the key elements of negotiation can help you secure a favorable outcome.

1. Know Your Objectives

Before entering any negotiation, it’s essential to define your objectives clearly. What are you hoping to achieve from this agreement? What are your non-negotiables? Having a well-defined list of objectives will guide your strategy and prevent you from making concessions that are detrimental to your interests.

2. Research and Preparation

Thorough research is critical. Investigate the other party’s business, their track record, and their potential motivations. Understanding their perspective will help you anticipate their arguments and develop counter-arguments.

Additionally, prepare a negotiation plan. This plan should outline your desired outcomes, potential concessions, and fallback positions. Having a plan in place provides structure and helps you stay focused during the negotiation process.

3. Active Listening and Communication

Effective communication is key. Listen actively to the other party’s concerns and perspectives. Ask clarifying questions to ensure you fully understand their position. Be clear and concise in expressing your own needs and priorities. Avoid making assumptions and always aim for mutual understanding.

4. Building Relationships

Negotiation is not just about winning; it’s also about building relationships. Treat the other party with respect and strive for a mutually beneficial outcome. Focus on finding common ground and solutions that address the needs of both parties. This approach can foster a more cooperative and long-lasting relationship.

5. Creative Problem-Solving

Negotiation often involves finding creative solutions to complex issues. Be open to exploring alternative options and compromise. Don’t be afraid to propose new ideas or suggest modifications to the original terms. The goal is to find a solution that satisfies everyone’s core needs.

6. Be Prepared to Walk Away

Even with meticulous preparation and negotiation skills, there may be times when an agreement is not possible. Have the courage to walk away from a deal if the terms are unfavorable or if the other party is unwilling to compromise. It’s better to walk away than to agree to something that will ultimately hurt your business or personal interests.

Negotiating the terms of an agreement is a valuable skill that can benefit individuals and businesses alike. By understanding the key elements of negotiation and employing effective strategies, you can increase your chances of achieving favorable outcomes and building strong relationships. Remember, successful negotiation requires a combination of knowledge, preparation, communication, and a willingness to compromise.

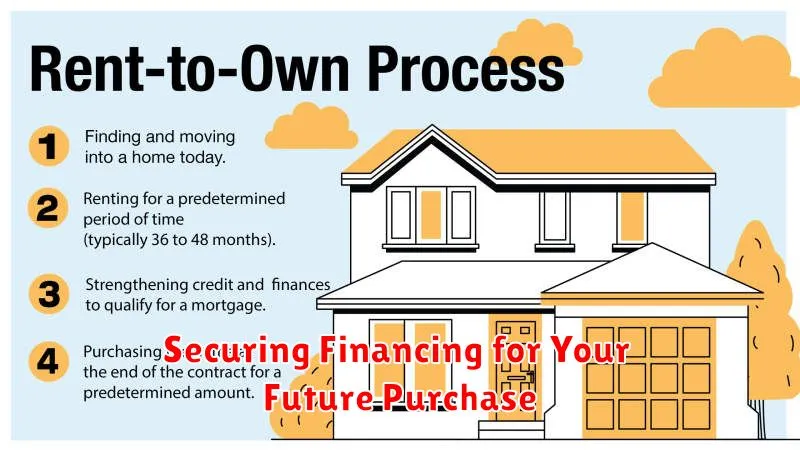

Securing Financing for Your Future Purchase

Financing a purchase, whether it’s a house, a car, or a big-ticket item, is a significant step in your financial journey. It’s crucial to understand the process and ensure you’re securing the best financing options available. This article will guide you through the essential steps for securing financing for your future purchase.

1. Assess Your Financial Situation

Before you start shopping for financing, it’s essential to get a clear picture of your financial standing. This includes determining your credit score, understanding your income and expenses, and calculating your debt-to-income ratio (DTI). A good credit score and a low DTI will make you more attractive to lenders and qualify you for better interest rates.

2. Shop Around for Lenders

Don’t settle for the first financing offer you receive. Take the time to compare rates and terms from multiple lenders, including banks, credit unions, and online lenders. It’s a good idea to get pre-approved for loans from several lenders, as this demonstrates to sellers that you’re a serious buyer and can help you secure a better price.

3. Understand Loan Terms

Each loan has different terms, such as the interest rate, loan term, and fees. Carefully review these terms and ask clarifying questions before signing any loan agreement. A lower interest rate and shorter loan term will result in lower overall costs, but may also require higher monthly payments.

4. Consider Your Payment Options

Think about your budget and choose a loan that fits comfortably within your monthly expenses. Don’t overextend yourself by taking on a loan you can’t afford. If you need a little extra flexibility, consider a loan with a variable interest rate, which can fluctuate over time.

5. Review and Sign the Loan Agreement

Before signing the loan agreement, carefully review all the terms and conditions. Ensure you understand all the fees involved and the repayment schedule. If you have any questions, ask your lender for clarification before signing.

Conclusion

Securing financing for your future purchase can be a daunting task, but by following these steps, you can navigate the process efficiently and confidently. Remember to prioritize your financial well-being, shop around for the best rates, and thoroughly understand the loan terms before making any commitments. By taking the time to do your research and plan accordingly, you can secure the financing you need to achieve your financial goals.

Legal and Financial Advice for Rent-to-Own

Rent-to-own agreements, also known as lease-purchase agreements, can be a tempting option for those who want to own a home but may not have the traditional financing requirements. However, it’s crucial to understand the legal and financial aspects before signing on the dotted line. This guide will provide valuable insights into what you need to know before embarking on a rent-to-own journey.

Understanding the Contract

The most important step is carefully reviewing the rent-to-own contract. This document outlines the terms of the agreement, including the purchase price, monthly rent, and the duration of the lease period. It’s essential to pay attention to:

- Purchase price: Is the price fair and comparable to similar properties in the area?

- Rent credit: How much of your monthly rent goes towards the purchase price? A higher percentage of rent applied to the purchase price is more beneficial.

- Option fee: This is a non-refundable fee paid upfront to secure the option to purchase the property. Ensure the fee is reasonable.

- Termination clauses: Understand the conditions under which you can terminate the agreement and whether you’ll receive any refund of the option fee.

- Inspection clause: Determine if the agreement allows for a professional inspection of the property before the purchase.

Financial Considerations

It’s crucial to assess your financial readiness before entering a rent-to-own agreement. Consider these factors:

- Credit score: Your credit score will play a significant role in your ability to secure financing for the final purchase. Improve your credit score before embarking on the agreement.

- Savings: Have enough savings for the down payment, closing costs, and potential repairs or improvements.

- Income: Ensure your income is sufficient to cover the monthly rent, other expenses, and the eventual mortgage payments.

- Market conditions: Research the real estate market in the area to ensure the purchase price remains competitive and that you’re not overpaying.

Legal Guidance

Consider consulting with a real estate attorney to review the contract and ensure it’s fair and protects your interests. An attorney can:

- Negotiate favorable terms: Help you negotiate better purchase price, rent credit, and other crucial terms.

- Identify potential risks: Highlight any potential pitfalls in the contract and provide legal counsel.

- Protect your rights: Ensure the contract complies with all local and state laws and regulations.

Final Thoughts

Rent-to-own agreements can be an appealing option for homeownership. However, understanding the legal and financial aspects, including the contract terms, your financial situation, and the potential risks, is crucial. Consulting with legal professionals and experts can empower you to make informed decisions and navigate this path confidently.

{kind=link}