Are you tired of paying rent and want to build equity? Or maybe you’re wondering if renting is actually the smarter financial move? Deciding whether to rent an apartment or buy a home is a huge decision that can impact your finances for years to come. There are many factors to consider, including your financial situation, lifestyle, and personal goals. This article will delve into the pros and cons of each option, helping you weigh your options and make the right choice for you.

Analyzing Your Financial Situation and Readiness

Before embarking on any financial journey, it’s crucial to assess your current financial situation and readiness. This involves understanding your income, expenses, assets, and liabilities. A clear picture of your financial health will guide you in setting realistic goals and making informed decisions.

Start by creating a budget. Track your income and expenses for a few months to identify areas where you can save money. Consider using budgeting apps or spreadsheets for easy tracking. Once you have a comprehensive budget, you can determine your net income (income minus expenses). This figure represents the amount of money you have available for savings, debt repayment, and other financial goals.

Next, evaluate your assets, which are anything you own that has value, such as your house, car, investments, and savings accounts. Then, assess your liabilities, which are your outstanding debts, including mortgages, loans, and credit card balances.

Once you have a clear understanding of your income, expenses, assets, and liabilities, you can calculate your net worth, which is the difference between your assets and liabilities. A positive net worth indicates financial strength, while a negative net worth suggests a need for improvement.

Finally, assess your financial readiness. This involves evaluating your ability to manage your money effectively, make sound financial decisions, and reach your financial goals. Consider factors such as your financial literacy, credit score, and emergency fund.

By taking the time to analyze your financial situation and readiness, you can gain valuable insights into your current financial position and develop a solid foundation for achieving your financial aspirations.

Comparing the Costs of Renting vs. Owning

The age-old debate of renting vs. owning a home is one that has captivated homeowners and renters alike for decades. While both options present distinct advantages and disadvantages, understanding the financial implications is crucial when making this significant life decision.

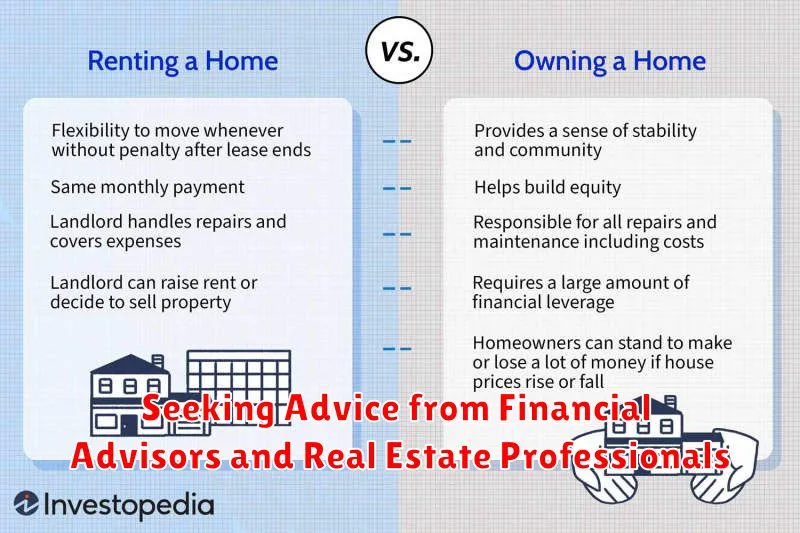

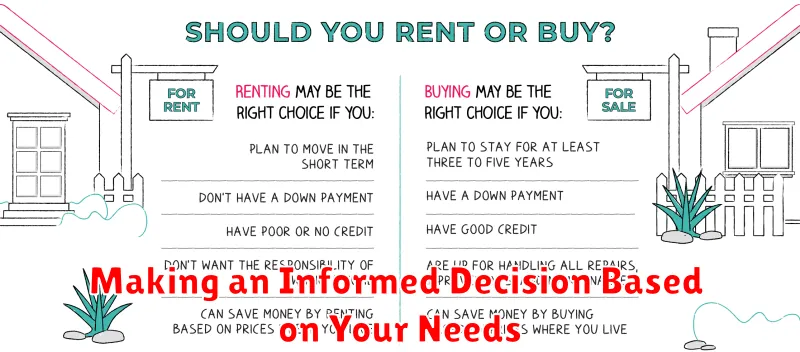

Renting: Flexibility and Low Upfront Costs

Renting offers several benefits, primarily flexibility and low upfront costs. Renters can typically move more easily, as they are not tied down by a mortgage or property maintenance responsibilities. Additionally, the initial financial investment is significantly lower, requiring only a security deposit and first month’s rent. However, renters may face limitations in customizing their living space and potential rent increases over time.

Owning: Building Equity and Long-Term Investment

Owning a home provides a sense of stability and allows for building equity over time. As you make mortgage payments, your ownership stake in the property increases. Homeownership also offers tax benefits, such as deductions for mortgage interest and property taxes. However, owning a home comes with significant upfront costs, including a down payment, closing costs, and ongoing maintenance expenses.

Financial Factors to Consider

When comparing the costs of renting vs. owning, it is essential to consider several key financial factors:

- Mortgage payments vs. rent: Compare the monthly cost of renting to the estimated mortgage payment, including principal, interest, taxes, and insurance.

- Property taxes and insurance: Homeowners are responsible for paying property taxes and homeowners insurance, which can add to monthly expenses.

- Maintenance costs: Owning a home involves ongoing maintenance expenses, such as repairs, landscaping, and utilities.

- Opportunity cost: Consider the opportunity cost of your down payment. Would that money be better invested elsewhere?

Conclusion

The decision to rent or buy is a personal one, and the best choice depends on individual circumstances and financial goals. By carefully evaluating the pros and cons of each option and considering the factors outlined above, you can make an informed decision that aligns with your needs and aspirations.

Assessing Your Lifestyle and Long-Term Plans

Assessing your lifestyle and long-term plans is an important step in achieving your goals and living a fulfilling life. By taking the time to reflect on your current situation and where you want to be in the future, you can gain valuable insights that can help you make informed decisions and create a plan for success.

What is Your Current Lifestyle?

Start by taking an honest look at your current lifestyle. Consider your daily routine, your work-life balance, your relationships, your health, and your finances. Are you happy with your current situation, or are there areas that you would like to improve?

What are Your Long-Term Goals?

Once you have a clear understanding of your current lifestyle, it’s time to start thinking about your long-term goals. What are your dreams and aspirations? What do you want to achieve in the next 5, 10, or even 20 years? Set realistic and achievable goals that align with your values and interests.

What are Your Priorities?

Your long-term goals should be aligned with your priorities. What is most important to you in life? Is it your family, your career, your health, or something else entirely? Once you know what your priorities are, you can start making choices that support them.

Create a Plan

After assessing your lifestyle and long-term plans, it’s time to create a plan of action. This plan should outline the steps you need to take to achieve your goals. Set realistic deadlines, break down large goals into smaller, more manageable tasks, and track your progress along the way.

Stay Flexible

Life is unpredictable, and your plans may need to change over time. Be open to adjusting your goals and strategies as needed. It’s important to be flexible and adapt to new circumstances.

Review Your Plan Regularly

Take some time each month to review your plan and make adjustments as necessary. This will help you stay on track and ensure that your goals are still aligned with your priorities.

Understanding the Responsibilities of Homeownership

Owning a home is a significant milestone in many people’s lives, offering a sense of stability, privacy, and pride. However, it’s crucial to understand that homeownership comes with a set of responsibilities that extend beyond simply making mortgage payments. Failing to fulfill these responsibilities can lead to financial strain, legal issues, and even the loss of your home.

Here are some key responsibilities of homeownership:

Financial Responsibilities

- Mortgage Payments: This is the primary financial obligation of homeownership. Making timely payments is essential to avoid late fees, penalties, and ultimately, foreclosure.

- Property Taxes: These taxes are levied by local governments and are used to fund public services. Failure to pay property taxes can lead to liens on your property, making it difficult to sell or refinance.

- Home Insurance: Homeowners insurance protects you from financial losses due to events like fire, theft, or natural disasters. It is typically a requirement for mortgage lenders.

- Utilities: You are responsible for paying for utilities such as electricity, gas, water, and sewage.

- Home Maintenance and Repairs: Routine maintenance and repairs are essential to keep your home in good condition. This includes tasks like cleaning gutters, inspecting the roof, and fixing leaky faucets.

- HOA Fees (if applicable): If you live in a homeowner’s association (HOA), you’ll need to pay monthly fees to cover common area maintenance and other services.

Maintenance and Repairs

Beyond financial responsibilities, you’re also responsible for maintaining and repairing your property. This includes:

- Landscaping: Maintaining a well-kept lawn and garden is crucial for curb appeal and property value.

- Roof Maintenance: Regular inspections and repairs are essential to prevent leaks and damage.

- Plumbing and Electrical: It’s important to address any plumbing or electrical issues promptly to avoid major problems and safety hazards.

- Pest Control: Regular pest control is important to prevent infestations and protect your home’s structure.

Legal Responsibilities

Homeownership also comes with legal responsibilities:

- Following Building Codes: You must comply with local building codes when making any additions or renovations to your property.

- Maintaining Safety: You are responsible for ensuring the safety of your property for yourself, your family, and visitors. This includes addressing potential hazards like trip hazards, faulty wiring, and unsecured stairs.

Understanding the Responsibilities

It’s essential to understand and embrace these responsibilities before making the leap into homeownership. Being financially prepared, responsible, and proactive with maintenance can help ensure a positive and rewarding homeownership experience.

Exploring the Benefits of Renting

In the realm of housing options, the choice between renting and owning often sparks spirited debate. While homeownership holds its allure, renting presents a compelling alternative, offering a host of benefits that cater to diverse lifestyles and financial situations.

One of the most significant advantages of renting is flexibility. Unlike homeowners, renters are not tied down to a fixed location for an extended period. This flexibility allows them to relocate more easily, whether for job opportunities, family matters, or simply a change of scenery. The ability to move without the hassle of selling a property provides renters with greater freedom and adaptability.

Another noteworthy benefit is financial freedom. Renters generally have lower upfront costs compared to homeowners. They do not have to shoulder the burden of a down payment, mortgage payments, property taxes, and insurance premiums. This financial flexibility allows renters to allocate their resources towards other goals, such as saving for retirement, travel, or education.

Renters also benefit from lower maintenance costs. Landlords are typically responsible for major repairs and upkeep of the rental property. This removes the financial burden and time commitment associated with homeownership, allowing renters to focus on their own pursuits. Moreover, renters do not have to worry about the unexpected costs of repairs or renovations.

Furthermore, renting offers amenities and services that may not be readily available to homeowners. Many rental properties come equipped with amenities such as swimming pools, fitness centers, and laundry facilities. These amenities enhance the quality of life and provide convenience for renters. Some landlords even offer additional services, such as on-site maintenance or concierge services.

In conclusion, renting provides a compelling alternative to homeownership, offering a range of benefits that cater to diverse lifestyles and financial situations. From flexibility and financial freedom to lower maintenance costs and access to amenities, renting offers a compelling option for individuals seeking a hassle-free and adaptable housing solution.

Considering Market Conditions and Investment Potential

Investing can be a daunting task, especially in today’s volatile market. It’s crucial to consider current market conditions and investment potential before making any decisions. By understanding the factors influencing the market, you can make informed choices that align with your financial goals.

Understanding Market Conditions

Market conditions are influenced by a range of factors, including economic growth, interest rates, inflation, and global events. It’s important to stay informed about these factors and their potential impact on your investments. For example, rising interest rates can lead to lower stock prices, while economic growth can boost the value of your investments.

Assessing Investment Potential

Once you understand the current market conditions, you can begin to assess the potential of different investment options. This involves researching companies, sectors, and asset classes, and considering factors such as their financial performance, future growth prospects, and risk profiles. You can also consult with a financial advisor to get personalized guidance.

Diversification for Risk Management

Diversification is a key principle of investing. By spreading your investments across different asset classes, you can reduce your overall risk. This means investing in a mix of stocks, bonds, real estate, and other assets, each with varying levels of risk and potential returns.

Long-Term Perspective

Investing is a long-term game. Don’t get discouraged by short-term market fluctuations. Instead, focus on your long-term goals and stay invested through market cycles. Regularly review your portfolio and make adjustments as needed to ensure it aligns with your goals.

Conclusion

Considering market conditions and investment potential is essential for making informed investment decisions. By understanding the factors influencing the market, assessing the potential of different investment options, and practicing diversification, you can position yourself for long-term success.

Weighing the Tax Implications of Both Options

It’s crucial to consider the tax implications of your choices. Here’s a breakdown of how each option could affect your tax situation:

Option 1: Buying a Home

Owning a home brings certain tax benefits, but it also comes with its fair share of potential tax liabilities. Here’s a closer look:

Benefits:

- Mortgage Interest Deduction: This deduction allows homeowners to reduce their taxable income by the amount of interest paid on their mortgage. This can result in significant tax savings, especially in the early years of the mortgage when interest payments are higher.

- Property Tax Deduction: The deduction for property taxes can also lower your taxable income. However, this deduction is subject to limitations, so it’s essential to consult with a tax professional for personalized guidance.

Liabilities:

- Capital Gains Tax: If you sell your home for a profit (i.e., sell it for more than your original purchase price plus any improvements), you’ll likely owe capital gains tax. However, you may be eligible for a tax exemption if you meet certain conditions.

- Property Taxes: Depending on your location, property taxes can be a substantial expense. These taxes are typically assessed annually and are based on the value of your property.

- Homeowners Insurance: Protecting your investment with homeowners insurance is crucial. While not directly considered a tax liability, the cost of this insurance can add to your overall housing expenses.

Option 2: Renting

Renting offers a different set of tax implications. While it generally doesn’t provide the same tax benefits as homeownership, there are some potential advantages.

Benefits:

- No Property Taxes: Renters are typically not responsible for paying property taxes. This can be a significant cost savings compared to homeownership.

- Flexibility: Renting offers greater flexibility. If your job or lifestyle changes, you can move more easily compared to selling a home.

Liabilities:

- No Tax Deductions: In most cases, rent payments are not tax-deductible.

- Rent Increases: Renters may face the possibility of rent increases, which can impact their budget.

- Limited Control: As a renter, you have less control over your living space. Landlords may have restrictions on modifications or improvements.

Ultimately, the best option for you depends on your individual circumstances. It’s crucial to consult with a financial advisor and tax professional to determine the most tax-efficient path based on your financial goals and income.

Seeking Advice from Financial Advisors and Real Estate Professionals

Navigating the complex world of finance and real estate can be daunting, especially for those without prior experience or knowledge. In such situations, seeking advice from qualified professionals is crucial to making informed decisions and achieving financial success.

Financial Advisors

Financial advisors provide guidance on various aspects of personal finance, including:

- Investment planning: Selecting appropriate investments based on risk tolerance and financial goals.

- Retirement planning: Developing a strategy to ensure financial security during retirement.

- Tax planning: Minimizing tax liabilities through legal strategies.

- Estate planning: Preparing for the distribution of assets after death.

When choosing a financial advisor, it’s essential to consider their qualifications, experience, and fees. Look for a Certified Financial Planner (CFP®) or a Chartered Financial Analyst (CFA) who can provide personalized advice.

Real Estate Professionals

Real estate professionals, such as real estate agents and brokers, offer expertise in buying, selling, and managing properties. Their services include:

- Market analysis: Providing insights into local real estate trends and pricing.

- Property search and negotiation: Identifying suitable properties and negotiating favorable terms.

- Property management: Overseeing rental properties and tenant relationships.

Choosing the right real estate professional is crucial for a successful real estate transaction. Seek out agents with a proven track record, strong negotiation skills, and a deep understanding of the local market.

Benefits of Professional Advice

Consulting with financial advisors and real estate professionals offers numerous benefits, including:

- Objective perspective: Professionals can provide unbiased advice based on your individual circumstances.

- Expertise and experience: They possess specialized knowledge and insights into the intricacies of finance and real estate.

- Time savings: They can handle complex tasks and research, freeing up your time for other pursuits.

- Peace of mind: Knowing you have qualified professionals on your side can reduce stress and anxiety.

Seeking advice from qualified professionals can be a valuable investment that can help you make informed decisions, achieve your financial goals, and build a secure future.

Making an Informed Decision Based on Your Needs

In today’s world, we are bombarded with choices. From what we eat to what we buy, there are countless options available to us. This can be overwhelming at times, but it’s also a great opportunity to make informed decisions that are right for us. The key is to understand our needs and preferences, and then carefully evaluate the options before making a choice.

Consider your needs: The first step is to identify your needs. What are you looking for in this particular decision? What are your priorities? For example, if you are buying a new car, your needs might include fuel efficiency, safety features, cargo space, and affordability.

Do your research: Once you know your needs, it’s time to start researching your options. This can include reading reviews, comparing features, and talking to others who have experience with similar products or services. This step is crucial to gaining valuable insights and ensuring you make the best decision possible.

Evaluate your options: With a good understanding of your needs and a solid research base, you can now evaluate your options more effectively. Compare the features and benefits of each option and weigh them against your priorities.

Consider the long-term impact: Don’t just focus on the immediate benefits. Think about the long-term impact of your decision. For example, if you are choosing a new phone, consider the lifespan of the battery, the availability of software updates, and the overall durability of the device.

Trust your gut: After careful consideration, trust your gut instinct. If something feels off or doesn’t sit right with you, it’s probably best to reconsider.

Making an informed decision is a process that takes time and effort. However, by following these steps, you can increase your chances of making a choice that you are happy with. Ultimately, it is about understanding your needs, researching your options, and making a decision that is right for you.

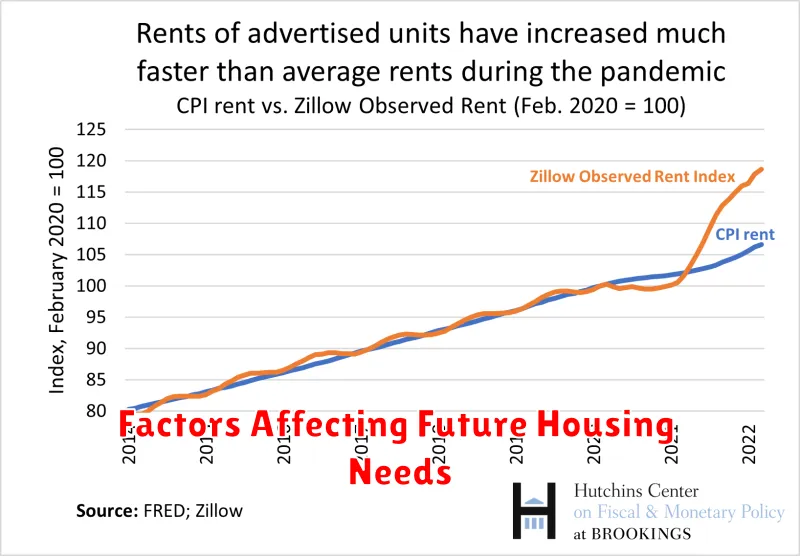

Factors Affecting Future Housing Needs

The housing market is constantly evolving, influenced by a complex interplay of factors that shape future housing needs. Understanding these factors is crucial for policymakers, developers, and individuals alike, as it allows for informed decision-making and preparation for the housing landscape of tomorrow.

Demographic Shifts

Population growth, aging populations, and changing household compositions are significant drivers of housing demand. Urbanization is a global trend, leading to increased demand for housing in cities. As populations age, the need for accessible and adaptable housing rises. The increasing prevalence of single-person households and multi-generational families also influences housing preferences.

Economic Conditions

Economic factors, such as employment rates, income levels, and interest rates, play a pivotal role in shaping housing affordability and demand. Strong economic growth can stimulate demand for housing, while economic downturns can lead to reduced demand and affordability challenges. Rising housing costs can create affordability issues, particularly for lower-income households.

Technological Advancements

Technological advancements are transforming the housing sector, influencing design, construction, and living experiences. Smart homes, energy-efficient technologies, and digital connectivity are shaping future housing needs. These advancements can lead to more sustainable, comfortable, and convenient living environments.

Environmental Concerns

Growing awareness of environmental issues has led to a demand for sustainable and eco-friendly housing. This includes energy-efficient buildings, green building materials, and sustainable land use practices. As climate change concerns escalate, the need for resilient and adaptable housing solutions becomes increasingly important.

Social and Cultural Trends

Social and cultural trends also influence housing preferences. Shared living, co-housing, and intentional communities are gaining popularity as alternative living arrangements. Changing preferences for walkability, access to public spaces, and community engagement are shaping urban planning and housing development.

Government Policies

Government policies, such as zoning regulations, building codes, and housing subsidies, have a profound impact on housing availability, affordability, and development patterns. Policies promoting affordable housing, sustainable development, and housing diversity can address the challenges of the future housing market.

By considering these diverse factors, policymakers, developers, and individuals can make informed decisions to meet the evolving housing needs of the future. Understanding these trends can facilitate a more sustainable, equitable, and adaptable housing landscape for generations to come.

{kind=link}