Are you tired of throwing money away on rent each month and dreaming of building equity in your own home? Transitioning from renting to homeownership can be a daunting but rewarding journey. This comprehensive guide will walk you through the essential steps, from understanding your finances to navigating the mortgage process. Whether you’re a first-time buyer or looking to upgrade, we’ll equip you with the knowledge and strategies to make your homeownership dreams a reality.

Assessing Your Financial Readiness for Homeownership

Buying a home is a significant financial commitment, and it’s crucial to assess your financial readiness before taking the plunge. A well-planned approach can help you avoid financial strain and ensure a smooth homeownership journey.

1. Determine Your Budget

Before starting your home search, it’s essential to establish a clear budget. Consider your income, expenses, and savings. A good rule of thumb is to aim for a monthly mortgage payment that’s no more than 28% of your gross monthly income. Don’t forget to factor in additional costs such as property taxes, homeowners insurance, and potential maintenance expenses.

2. Check Your Credit Score

Your credit score plays a vital role in securing a mortgage loan. Lenders use your credit score to determine your creditworthiness and the interest rate they’ll offer you. A higher credit score typically translates to lower interest rates, which can save you thousands of dollars over the life of your loan. It’s recommended to check your credit score regularly and take steps to improve it if necessary.

3. Save for a Down Payment

A down payment is a substantial upfront cost for buying a home. The standard down payment is 20% of the purchase price, but you may be able to secure a loan with a lower down payment depending on the type of mortgage you choose. Start saving for your down payment as early as possible, and consider utilizing a high-yield savings account or other investment options to maximize your returns.

4. Understand Closing Costs

In addition to the down payment, there are closing costs associated with buying a home. These costs can range from 2% to 5% of the purchase price and include fees for things like loan origination, title insurance, and property taxes. Be sure to budget for these expenses to avoid surprises during the closing process.

5. Assess Your Emergency Fund

Having an emergency fund is crucial for any homeowner. Unexpected repairs, maintenance issues, or job loss can arise, and having a financial safety net can help you avoid going into debt or selling your home prematurely. Aim to have at least three to six months of living expenses saved in an emergency fund.

6. Get Pre-Approved for a Mortgage

Getting pre-approved for a mortgage before you start shopping for a home is a smart move. A pre-approval gives you a clear picture of how much you can afford to borrow, and it makes you a more competitive buyer. It demonstrates to sellers that you’re financially ready to purchase their home.

7. Seek Financial Advice

If you’re unsure about your financial readiness for homeownership, don’t hesitate to seek financial advice from a qualified professional. A financial advisor can help you assess your situation, develop a financial plan, and guide you through the home buying process.

By taking these steps to assess your financial readiness, you can approach homeownership with confidence and ensure a smooth and successful experience.

Saving for a Down Payment While Renting

Saving for a down payment while renting can seem like an uphill battle, but it’s definitely possible. It’s about making smart financial choices and finding ways to maximize your savings potential.

There are several factors that contribute to the difficulty of saving for a down payment while renting, including:

- Rent Costs: Rent can be a significant expense, especially in high-cost areas. This leaves less money available for saving.

- Lifestyle Expenses: It’s easy to overspend on non-essential items when you’re not facing the same financial pressures as homeowners.

- Lack of Equity Building: Unlike homeowners, renters don’t build equity in their homes, which can be a source of funds for future purchases.

However, there are effective strategies you can employ to overcome these challenges:

1. Create a Realistic Budget

The first step is to understand where your money is going. Track your spending for a few months to identify areas where you can cut back. Consider using a budgeting app or spreadsheet to track your income and expenses.

2. Set SMART Goals

Having clear goals helps you stay motivated. Determine how much you need for a down payment, and set realistic timelines for reaching that goal. Break down your savings goal into smaller, more manageable chunks.

3. Increase Your Income

If your income is limited, consider ways to earn extra money. Take on a side hustle, sell unused items, or ask for a raise at work. Every bit helps!

4. Automate Your Savings

Set up automatic transfers from your checking account to your savings account. This ensures that you’re consistently saving, even if you forget about it.

5. Look for Housing Options

Consider moving to a less expensive neighborhood or finding a roommate to reduce your rent expenses. This frees up more money to allocate towards your savings goals.

6. Take Advantage of Employer-Sponsored Programs

If your employer offers a 401(k) or other retirement savings plan, take advantage of any matching contributions they offer. This effectively increases your savings by matching your contributions.

Saving for a down payment while renting requires discipline and commitment. But by taking advantage of these strategies, you can pave the way for a brighter financial future and the home of your dreams.

Understanding Mortgage Options and Pre-Approval

Buying a home is a significant financial decision, and understanding your mortgage options is crucial. A mortgage is a loan that allows you to purchase a property, with the property itself serving as collateral. There are various mortgage options available, each with its own features, terms, and costs.

Before you begin your home search, it’s essential to get pre-approved for a mortgage. Pre-approval is a process where a lender reviews your financial information and provides an estimate of how much you can borrow. This gives you a clear picture of your buying power and helps you avoid wasting time looking at homes that are out of your price range.

Types of Mortgages

Some common types of mortgages include:

- Fixed-rate mortgages: These mortgages have an interest rate that remains constant for the life of the loan, offering predictable monthly payments.

- Adjustable-rate mortgages (ARMs): These mortgages have an interest rate that can fluctuate based on a predetermined index. They may offer lower initial rates but could result in higher payments in the future.

- Conventional loans: These mortgages are not backed by the government and typically require a down payment of 20% or more.

- Government-backed loans: These mortgages are insured or guaranteed by government agencies such as the Federal Housing Administration (FHA), the Veterans Affairs (VA) Department, or the United States Department of Agriculture (USDA). They often have lower down payment requirements and more flexible guidelines.

Factors Affecting Mortgage Rates

Mortgage rates are influenced by various factors, including:

- Credit score: A higher credit score generally leads to lower interest rates.

- Loan amount: Larger loan amounts often come with higher rates.

- Loan term: Longer loan terms typically have lower monthly payments but may result in higher overall interest costs.

- Market conditions: Interest rates fluctuate based on economic factors.

Getting Pre-Approved

To get pre-approved, you’ll need to provide the lender with your financial information, including your income, assets, and credit history. The lender will use this information to determine your creditworthiness and estimate the amount you can borrow.

Benefits of Pre-Approval

Pre-approval offers several benefits:

- Confidence in your buying power: You’ll know how much you can afford to spend on a home.

- Stronger negotiating position: Sellers are more likely to take you seriously as a buyer when you’re pre-approved.

- Faster closing process: Pre-approval can streamline the loan process and help you close on your home more quickly.

Choosing the Right Mortgage

Selecting the right mortgage is a personal decision that depends on your individual circumstances and financial goals. It’s advisable to consult with a mortgage professional to discuss your options and find the best fit for your needs.

Exploring Government Programs and Assistance

Navigating the complexities of government programs and assistance can feel overwhelming, but it doesn’t have to be. Understanding the resources available to you can make a significant difference in your life, whether you’re facing financial challenges, need healthcare support, or simply want to improve your well-being. This article serves as a guide to explore the various government programs and assistance options available to you.

Understanding Your Eligibility

The first step to accessing government programs and assistance is determining your eligibility. Each program has specific criteria, including factors like age, income, family size, and residency. It’s essential to gather all necessary documentation, such as your Social Security number, income verification, and proof of residency. The USA.gov website is an excellent resource for navigating government programs and their eligibility requirements.

Types of Government Assistance

Government programs and assistance encompass a wide range of categories, including:

- Financial Assistance: Programs like SNAP (food stamps), TANF (Temporary Assistance for Needy Families), and housing assistance provide financial support to individuals and families facing financial hardship.

- Healthcare Assistance: Medicaid, Medicare, and the Children’s Health Insurance Program (CHIP) offer affordable or free healthcare coverage to low-income individuals and families.

- Education Assistance: Federal student loans, Pell Grants, and other financial aid programs can help students afford college tuition and expenses.

- Job Training and Employment Assistance: Government programs like Workforce Innovation and Opportunity Act (WIOA) offer job training, employment placement services, and career counseling to help individuals gain new skills and find jobs.

- Disaster Relief and Emergency Assistance: In times of natural disasters or emergencies, government agencies provide financial assistance, housing assistance, and other support to affected individuals and families.

How to Apply

Application processes vary depending on the specific program. You can apply online, by phone, or in person at local government offices or community resource centers. Many programs offer online applications, making it convenient to apply from the comfort of your home. Ensure you gather all required documentation before starting the application process.

Additional Resources

Beyond government websites, various organizations and resources can help you navigate government programs and assistance. These resources include:

- Local Social Services Agencies: These agencies can provide information, referrals, and assistance with applying for government programs.

- Community Action Agencies: These agencies offer various programs and services to low-income families and individuals.

- Nonprofit Organizations: Many nonprofit organizations provide financial assistance, legal aid, and other support services to individuals and families in need.

By understanding your eligibility, exploring the available programs, and seeking assistance from trusted resources, you can leverage government programs and assistance to improve your financial stability, access healthcare, pursue education, and enhance your overall well-being.

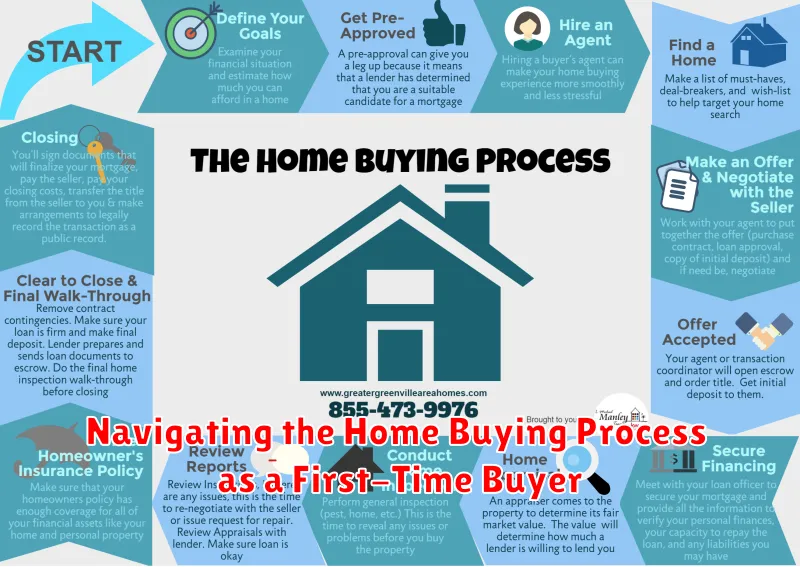

Navigating the Home Buying Process as a First-Time Buyer

Purchasing a home is a significant milestone in life, and for first-time buyers, the process can seem daunting. From understanding mortgage options to navigating negotiations, there are numerous steps involved. This comprehensive guide will equip you with the knowledge and tools you need to successfully navigate the home buying journey.

1. Assess Your Financial Situation

Before embarking on your home search, it’s crucial to assess your financial readiness. Determine your budget, taking into account your income, expenses, and debt obligations. Consider factors like property taxes, homeowners insurance, and potential maintenance costs. Get pre-approved for a mortgage from a lender to understand your borrowing power. This pre-approval demonstrates your financial seriousness to sellers.

2. Define Your Needs and Wants

Clearly define your housing needs and wants. Consider factors like location, size, number of bedrooms and bathrooms, and desired amenities. Prioritize your requirements and be realistic about what you can afford. Research different neighborhoods and explore their amenities, schools, and commute times to identify areas that align with your lifestyle.

3. Work with a Real Estate Agent

Partnering with an experienced real estate agent is highly recommended. They possess in-depth market knowledge, negotiation skills, and access to listings that may not be publicly available. A good agent will guide you through the entire process, from property searches to closing. They will also advocate for your best interests throughout negotiations.

4. Start Your Home Search

Armed with your financial understanding and defined needs, you can begin searching for homes. Utilize online real estate portals, attend open houses, and schedule private showings. As you view properties, carefully evaluate their condition, consider potential renovation costs, and assess their alignment with your requirements.

5. Making an Offer

When you find a home that suits your needs, you’ll need to submit an offer. Your real estate agent will help you craft a competitive offer that includes the purchase price, closing date, and any contingencies. Be prepared to negotiate, and don’t be afraid to walk away if the terms aren’t favorable.

6. Home Inspection and Appraisal

Once your offer is accepted, you’ll need to schedule a home inspection to assess the property’s condition. This inspection identifies any potential problems that could affect your purchase. An appraisal is also necessary to determine the fair market value of the home for lending purposes.

7. Closing and Moving

After the inspections and appraisals are complete, you’ll enter the closing process. This involves finalizing the loan, signing legal documents, and transferring ownership of the property. Once the closing is complete, you’ll have the keys to your new home and can start the process of moving in.

8. Enjoy Your New Home!

Congratulations on becoming a homeowner! After all the hard work and preparation, you can finally enjoy your new home. Remember to stay organized with your finances, schedule regular maintenance, and build a strong foundation for your future in your new space.

Making the Transition from Tenant to Homeowner

The dream of owning a home is a common one, but it can feel like an insurmountable task. Many people live in rented properties for years, unsure of how to make the leap to homeownership. If you’re ready to take the plunge, here are some tips to help make the transition smoother.

Financial Planning

The first step is to get your finances in order. This means getting pre-approved for a mortgage, which will give you a better idea of how much you can afford. Make sure to account for not only the mortgage payment but also property taxes, insurance, and potential maintenance costs. You’ll also need to save up for a down payment, which is typically around 20% of the purchase price.

Once you have a good grasp of your finances, it’s time to start shopping for a home. Work with a real estate agent who can help you find properties that meet your needs and budget. Be prepared to make compromises and be flexible in your search. You might not get everything on your wish list, but finding a place you can afford and enjoy is the most important thing.

Prepare for Homeownership

Once you’ve found a home and closed on the purchase, you’ll need to get ready for the responsibilities of homeownership. This includes learning about home maintenance and repair, as well as understanding your rights and responsibilities as a homeowner.

One of the most important things to do is to create a budget for homeownership. This should include all of your monthly expenses, such as your mortgage payment, property taxes, homeowners insurance, utilities, and any other costs associated with your home. It’s also a good idea to set aside some money each month for emergency repairs and maintenance.

You’ll also need to get familiar with the basics of home maintenance. This includes tasks such as changing air filters, cleaning gutters, and making minor repairs. If you’re not handy, you can always hire a professional to do these tasks for you.

Finally, it’s important to understand your rights and responsibilities as a homeowner. This includes things like property taxes, homeowner’s insurance, and the right to make changes to your property. Be sure to familiarize yourself with local laws and regulations.

Enjoy the Journey

Owning a home is a big responsibility, but it’s also a rewarding experience. You’ll have the freedom to personalize your space and build equity over time. Enjoy the process and don’t be afraid to ask for help when you need it. From your mortgage lender to your local hardware store, there are many resources available to support you as you navigate this exciting journey.

Tips for a Smooth Transition to Home Ownership

Owning a home is a significant milestone in life, offering a sense of stability and independence. However, the transition from renting to owning can be overwhelming. To ensure a smooth transition, it’s crucial to plan and prepare. Here are some tips to help you navigate the process with ease.

1. Get Pre-Approved for a Mortgage

Before you start house hunting, get pre-approved for a mortgage. This gives you a clear idea of how much you can afford to borrow and makes you a more serious buyer. It also demonstrates to sellers that you are financially capable of purchasing their home.

2. Set a Realistic Budget

When creating your budget, don’t forget to factor in closing costs, property taxes, insurance, and potential maintenance expenses. These costs can quickly add up, so it’s essential to be prepared.

3. Work with a Real Estate Agent

A real estate agent can be an invaluable resource during the home buying process. They can guide you through negotiations, help you find properties that meet your needs, and ensure a smooth transaction.

4. Understand the Closing Process

The closing process involves several steps, including signing documents, transferring ownership, and finalizing financing. It’s essential to understand each step and ask questions if you have any concerns.

5. Be Prepared for Unexpected Expenses

Even with careful planning, there may be unexpected expenses that arise during the home buying process. It’s wise to have a contingency fund in place to cover these costs.

6. Get Homeowner’s Insurance

Homeowner’s insurance is essential to protect your investment. It provides coverage for damage to your property and liability in case of accidents.

7. Make Home Improvements Gradually

Avoid making significant home improvements immediately after purchasing. Instead, focus on addressing essential repairs and gradually make upgrades over time.

8. Enjoy Your New Home

Once the transition is complete, take time to appreciate your new home. This is a significant accomplishment, so celebrate your success and enjoy the benefits of homeownership.

{kind=link}